Multivariate Forecasting with DeepAR#

This notebook outlines the application of DeepAR, a recently-proposed transformer-based model for time series forecasting, to a Electricity Consumption Dataset. The dataset contains the hourly electricity consumption of 321 customers from 2012 to 2014.

This demo uses an implementation of DeepAR from the PyTorch Forecasting package. PyTorch Forecasting is a package/repository that provides convenient implementations of several leading deep learning-based forecasting models, namely Temporal Fusion Transformers, N-BEATS, and DeepAR. PyTorch Forecasting is built using PyTorch Lightning, making it easier to train in multi-GPU compute environments, out-of-the-box.

Package Imports and Global Variables#

Note for Colab users: Run the following cell to install PyTorch Forecasting. After installation completes, you will likely need to restart the Colab runtime. If this is the case, a button RESTART RUNTIME will appear at the bottom of the next cell’s output.

if 'google.colab' in str(get_ipython()):

!pip install pytorch-forecasting==0.10.3

!pip install pytorch-lightning==1.5.9

!pip install torch==1.11.0 torchaudio==0.11.0 torchtext==0.6.0 torchvision==0.12.0

import os

import warnings

import pandas as pd

import matplotlib.pyplot as plt

import numpy as np

import torch

import pytorch_lightning as pl

from pytorch_forecasting.data import NaNLabelEncoder

from pytorch_lightning.callbacks import EarlyStopping

from pytorch_forecasting.metrics import NormalDistributionLoss

from pytorch_forecasting import TimeSeriesDataSet, Baseline, DeepAR, GroupNormalizer, MultiNormalizer, EncoderNormalizer

from sklearn.metrics import mean_squared_error, mean_absolute_error, mean_absolute_percentage_error

if 'google.colab' in str(get_ipython()):

from google.colab import drive

drive.mount('/content/drive')

warnings.filterwarnings("ignore")

DATA_PATH = "/ssd003/projects/forecasting_bootcamp/bootcamp_datasets/electricity/electricity.csv" # Will have to update dataset path if not running on Vector Cluster

EPOCHS = 1

VAL_PERC = .1

TEST_PERC = .005

BATCH_SIZE = 32

LAG_TIME = 30

LEAD_TIME = 30

Load Data#

We start by loading the data from a CSV file from DATA_PATH into a dataframe. Each column of the dataframe is a different time series that measures the hourly electricity consumption of one of the 320 households included in the dataset. Additonally, there is also a column that encodes the date and time of the observations. The last column, OT, is dropped as it is not relevant for this demo.

# Load CSV into dataframe and format

df = pd.read_csv(DATA_PATH, index_col=0)

df = df.iloc[:, :-1]

df.index = pd.to_datetime(df.index)

df = df.reset_index().rename({'index':'date'}, axis=1)

df

| date | 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | ... | 310 | 311 | 312 | 313 | 314 | 315 | 316 | 317 | 318 | 319 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 2016-07-01 02:00:00 | 14.0 | 69.0 | 234.0 | 415.0 | 215.0 | 1056.0 | 29.0 | 840.0 | 226.0 | ... | 199.0 | 676.0 | 372.0 | 80100.0 | 4719.0 | 5002.0 | 48.0 | 38.0 | 1558.0 | 182.0 |

| 1 | 2016-07-01 03:00:00 | 18.0 | 92.0 | 312.0 | 556.0 | 292.0 | 1363.0 | 29.0 | 1102.0 | 271.0 | ... | 265.0 | 805.0 | 452.0 | 95200.0 | 4643.0 | 6617.0 | 65.0 | 47.0 | 2177.0 | 253.0 |

| 2 | 2016-07-01 04:00:00 | 21.0 | 96.0 | 312.0 | 560.0 | 272.0 | 1240.0 | 29.0 | 1025.0 | 270.0 | ... | 278.0 | 817.0 | 430.0 | 96600.0 | 4285.0 | 6571.0 | 64.0 | 43.0 | 2193.0 | 218.0 |

| 3 | 2016-07-01 05:00:00 | 20.0 | 92.0 | 312.0 | 443.0 | 213.0 | 845.0 | 24.0 | 833.0 | 179.0 | ... | 271.0 | 801.0 | 291.0 | 94500.0 | 4222.0 | 6365.0 | 65.0 | 39.0 | 1315.0 | 195.0 |

| 4 | 2016-07-01 06:00:00 | 22.0 | 91.0 | 312.0 | 346.0 | 190.0 | 647.0 | 16.0 | 733.0 | 186.0 | ... | 267.0 | 807.0 | 279.0 | 91300.0 | 4116.0 | 6298.0 | 75.0 | 40.0 | 1378.0 | 191.0 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 26299 | 2019-07-01 21:00:00 | 11.0 | 116.0 | 8.0 | 844.0 | 384.0 | 1590.0 | 51.0 | 1412.0 | 407.0 | ... | 178.0 | 1897.0 | 1589.0 | 166500.0 | 9917.0 | 10412.0 | 324.0 | 21.0 | 1870.0 | 162.0 |

| 26300 | 2019-07-01 22:00:00 | 11.0 | 103.0 | 8.0 | 749.0 | 371.0 | 1366.0 | 47.0 | 1265.0 | 369.0 | ... | 241.0 | 1374.0 | 1336.0 | 158800.0 | 6812.0 | 8956.0 | 302.0 | 20.0 | 1506.0 | 438.0 |

| 26301 | 2019-07-01 23:00:00 | 12.0 | 93.0 | 8.0 | 650.0 | 346.0 | 1282.0 | 48.0 | 1079.0 | 308.0 | ... | 158.0 | 938.0 | 1311.0 | 154300.0 | 6602.0 | 5910.0 | 302.0 | 18.0 | 1864.0 | 621.0 |

| 26302 | 2019-07-02 00:00:00 | 10.0 | 92.0 | 8.0 | 646.0 | 349.0 | 1261.0 | 48.0 | 1009.0 | 288.0 | ... | 120.0 | 833.0 | 1227.0 | 141900.0 | 6546.0 | 5502.0 | 259.0 | 33.0 | 2623.0 | 783.0 |

| 26303 | 2019-07-02 01:00:00 | 11.0 | 88.0 | 8.0 | 648.0 | 337.0 | 1234.0 | 46.0 | 1005.0 | 261.0 | ... | 117.0 | 783.0 | 1089.0 | 112300.0 | 6188.0 | 4934.0 | 115.0 | 31.0 | 2706.0 | 647.0 |

26304 rows × 321 columns

Data Splitting#

The data is split sequentially into train, validation and test based on VAL_PERC and TEST_PERC global variables. We will withhold the last TEST_PERC of data for testing. In the code below, we are very careful to ensure that when training and validating the model, it does not have access to the withheld data.

n_samples = len(df)

n_val = int(n_samples * VAL_PERC)

n_test = int(n_samples * TEST_PERC)

n_train = n_samples - (n_val + n_test)

# Split data into train and test

train_df = df.iloc[:n_train, :]

val_df = df.iloc[n_train:n_train+n_val]

test_df = df.iloc[n_train+n_val:]

Data Formatting#

PyTorch Forecasting expects data to be formatted using its own TimeSeriesDataSet objects. Building a TimeSeriesDataSet begins with a Pandas DataFrame that we need to add certain custom columns.

PyTorch Forecasting models can accomodate datasets consisting of multiple, coincident time series in several ways. As per the documentation, a combination of group_id and time_idx identify a sample in the data, and that if we have only one time series, to set group_id to a constant. time_idx is an integer column denoting the time index. This, as opposed to the date column, is used to determine the temporal sequence of samples.

# Rename index to time_idx

train_df = train_df.reset_index().rename({'index':'time_idx'}, axis=1)

val_df = val_df.reset_index().rename({'index':'time_idx'}, axis=1)

test_df = test_df.reset_index().rename({'index':'time_idx'}, axis=1)

# Add group id column and initialize with 0

train_df['group_ids'] = 0

val_df['group_ids'] = 0

test_df['group_ids'] = 0

# Reshape data into single value column that is uniquely indexed by pairs of (time_idx, group_ids).

train_df = train_df.melt(id_vars=['time_idx', 'date'], value_vars=df.columns, var_name='group_ids')

val_df = val_df.melt(id_vars=['time_idx', 'date'], value_vars=df.columns, var_name='group_ids')

test_df = test_df.melt(id_vars=['time_idx', 'date'], value_vars=df.columns, var_name='group_ids')

Dataset Definition#

Now that we have the data in the format that TimeSeriesDataset expects, we can define the train_dataset, val_dataset and test_dataset. For each dataset, we can pass a number of parameters that specify the characteristics of the data and how it should be processed prior to being fed to the model. Some of the arguments include:

data: (pd.DataFrame) – dataframe with sequence data - each row can be identified withtime_idxand thegroup_idstarget: (Union[str, List[str]]) – column denoting the target or list of columns denoting the target - categorical or continous.max_encoder_length: (int) – maximum length to encode. This is the maximum history length used by the time series dataset.max_prediction_length: (int) – maximum prediction/decoder length (choose this not too short as it can help convergence)

For additional details in regards to the TimeSeriesDataset class, consult the PyTorch Forecasting Documentation.

# Define datasets

train_data = TimeSeriesDataSet(

data=train_df,

time_idx="time_idx",

target="value",

group_ids=['group_ids'],

max_encoder_length=LAG_TIME,

min_prediction_length=1,

max_prediction_length=LEAD_TIME,

categorical_encoders={"group_ids": NaNLabelEncoder().fit(train_df.group_ids)},

time_varying_unknown_reals=["value"],

time_varying_known_reals=["time_idx"],

target_normalizer=GroupNormalizer(groups=["group_ids"]),

)

val_data = TimeSeriesDataSet(

data=val_df,

time_idx="time_idx",

target="value",

group_ids=['group_ids'],

min_encoder_length=LAG_TIME,

max_encoder_length=LAG_TIME,

max_prediction_length=LEAD_TIME,

categorical_encoders={"group_ids": NaNLabelEncoder().fit(val_df.group_ids)},

time_varying_unknown_reals=["value"],

time_varying_known_reals=["time_idx"],

target_normalizer=GroupNormalizer(groups=["group_ids"]),

)

test_data = TimeSeriesDataSet(

data=test_df,

time_idx="time_idx",

target="value",

group_ids=['group_ids'],

min_encoder_length=LAG_TIME,

max_encoder_length=LAG_TIME,

max_prediction_length=LEAD_TIME,

categorical_encoders={"group_ids": NaNLabelEncoder().fit(test_df.group_ids)},

time_varying_unknown_reals=["value"],

time_varying_known_reals=["time_idx"],

target_normalizer=GroupNormalizer(groups=["group_ids"]),

)

# Define dataloaders

train_dataloader = train_data.to_dataloader(train=True, batch_size=BATCH_SIZE, num_workers=8)

val_dataloader = val_data.to_dataloader(train=False, batch_size=BATCH_SIZE, num_workers=8)

test_dataloader = test_data.to_dataloader(train=False, batch_size=BATCH_SIZE, num_workers=8)

Model#

DeepAR Overview#

DeepAR is an autoregressive recurrent neural network for probalistic time series forecasting. Similar to NBEATS, DeepAR learns a global model from historical data of one or more time series. The same model with shared parameters is used on both the conditioning range (input) as well as the prediction range (output) and consists of mutlti-layer recurrent neural network with LSTM cells. The output of the network is recursively generated one step at a time and consists of values (e.g. mean and standard deviation) that parametize a fixed distribution. The fixed distribution is specified by a likelihood function that is chosen to match the characteristics of the data. We can then obtain samples from the distribution to compute quantiles of interest over predictions. Some additional features of DeepAR include:

Robust: Handles time series of different magnitude as well as missing values

Flexible: Allows for covariates that are item dependent, time-dependent or both

Configurable: DeepAR allows us to specify any likelihood function as the output distribution as long as samples can easily be obtained and the log likelihood and gradients with respect to the parameters can be easily obtained

Model Definition#

Using the Pytorch Forecasting package, a DeepAR model can be easily initialized using the DeepAR.from_dataset method. This method constructs a DeepAR model using the characteristics of the TimeSeriesDataset that it is operating on. The arguments of the method include:

dataset: (TimeSeriesDataset) time series datasethidden_size: (int, optional) – hidden recurrent size - the most important hyperparameter along withrnn_layers. Defaults to 10.loss: (DistributionLoss, optional) – Distribution loss function. Keep in mind that each distribution loss function might have specific requirements for target normalization. Defaults toNormalDistributionLoss.

For additional details in regards to the DeepAR class, consult the PyTorch Forecasting Documentation.

# Init model with structure specified in dataset

net = DeepAR.from_dataset(

dataset=train_data,

hidden_size=32,

loss=NormalDistributionLoss(),

learning_rate=1e-4,

)

Training and Validation#

We first define a pytorch lighting trainer which encapsulates the training process and allows us to easily implement a training and validation loop with the specified parameters. The arguments to the trainer include:

max_epochs: (Optional[int]) – Stop training once this number of epochs is reached.limit_train_batches: (Union[int, float]) – How much of training dataset to check (float = fraction, int = num_batches).limit_val_batches: (Union[int, float]) – How much of validation dataset to check (float = fraction, int = num_batches).callbacks: (Union[List[Callback], Callback, None]) – Add a callback or list of callbacks.

Subsequently, we can use the fit method of the trainer with the net, train_dataloader and val_dataloader to perform the training and validation loop.

For more information regarding the pl.Trainer class, consult the PyTorch Lightning documentation.

# Set random seed

pl.seed_everything(42)

# Define early stopping criteria

early_stop_callback = EarlyStopping(monitor="val_loss", min_delta=1e-4, patience=10, verbose=False, mode="min")

# Init pytorch lightning trainer

trainer = pl.Trainer(

max_epochs=EPOCHS,

gpus=1,

gradient_clip_val=0.1,

callbacks=[early_stop_callback],

limit_train_batches=.2,

limit_val_batches=.2,

)

# Train and Validate Model

trainer.fit(

net,

train_dataloader=train_dataloader,

val_dataloaders=val_dataloader

)

Global seed set to 42

GPU available: True, used: True

TPU available: False, using: 0 TPU cores

IPU available: False, using: 0 IPUs

LOCAL_RANK: 0 - CUDA_VISIBLE_DEVICES: [0]

Set SLURM handle signals.

| Name | Type | Params

------------------------------------------------------------------

0 | loss | NormalDistributionLoss | 0

1 | logging_metrics | ModuleList | 0

2 | embeddings | MultiEmbedding | 0

3 | rnn | LSTM | 13.1 K

4 | distribution_projector | Linear | 66

------------------------------------------------------------------

13.1 K Trainable params

0 Non-trainable params

13.1 K Total params

0.052 Total estimated model params size (MB)

Global seed set to 42

Testing#

Visualize Predictions#

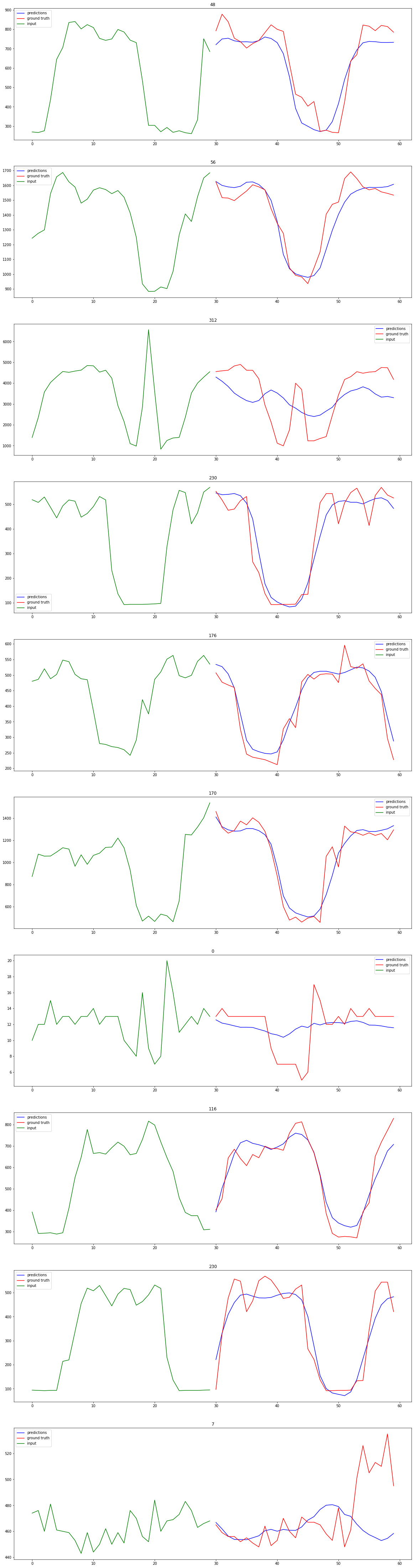

With the trained model from the previous step, we can apply it to the test set to get an unbias estimate of the models performance. Additionally, we can visualize the results to build some intuition about the forecasts being generated.

# Load best model from checkpoint

best_model_path = trainer.checkpoint_callback.best_model_path

best_model = DeepAR.load_from_checkpoint(best_model_path)

best_model = best_model.cuda()

# Get predictions from test dataset

preds = best_model.predict(test_dataloader, show_progress_bar=True)

# Aggregate inputs, ground truth and classes into tensor alligned with predictions

input_list, true_list, class_list = [], [], []

for x, y in test_dataloader:

input_list.append(x["encoder_target"])

true_list.append(y[0])

class_list.append(x["groups"])

inputs = torch.cat(input_list)

trues = torch.cat(true_list)

classes = torch.cat(class_list)

print(inputs.shape, preds.shape, trues.shape, classes.shape)

torch.Size([23040, 30]) torch.Size([23040, 30]) torch.Size([23040, 30]) torch.Size([23040, 1])

# Select indices of samples to visualize

n_samples = 10

ss_indices = np.random.choice(range(preds.shape[0]), n_samples, replace=False)

ss_pred = preds[ss_indices]

ss_true = trues[ss_indices]

ss_input = inputs[ss_indices]

ss_class = classes[ss_indices]

print(ss_input.shape, ss_pred.shape, ss_true.shape, ss_class.shape)

torch.Size([10, 30]) torch.Size([10, 30]) torch.Size([10, 30]) torch.Size([10, 1])

# Loop through samples and plot input, ground truth and prediction

f, axarr = plt.subplots(n_samples, 1, figsize=(20, 80))

for i in range(n_samples):

series_preds = ss_pred[i, :].squeeze()

series_trues = ss_true[i, :].squeeze()

series_inputs = ss_input[i, :].squeeze()

feat_name = str(ss_class[i].item())

input_len = series_inputs.shape[0]

pred_gt_len = series_preds.shape[0]

input_x = np.array([i for i in range(input_len)])

x = np.array([i for i in range(input_len, input_len+pred_gt_len)])

axarr[i].plot(x, series_preds, c="blue", label="predictions")

axarr[i].plot(x, series_trues, c="red", label="ground truth")

axarr[i].plot(input_x, series_inputs, c="green", label="input")

axarr[i].legend()

axarr[i].set_title(feat_name)

Quantitative Resutls#

To assess the performance of DeepAR on the dataset, we calculate its performance on the test set using a set of metrics that are commonly used in time series forecasting. The metrics include Mean Absolute Error (MAE) and Mean Squared Error (MSE).

# Calculate losses

mse = mean_squared_error(trues.cpu().numpy(), preds.cpu().numpy())

mae = mean_absolute_error(trues.cpu().numpy(), preds.cpu().numpy())

print(f"MSE: {mse} MAE: {mae}")

MSE: 1333233.5 MAE: 213.55343627929688